This post may contain affiliate links, which means I’ll receive a commission if you purchase through my links, at no extra cost to you. Please read full disclosure for more information.

Net Operating Income (NOI) is a metric used to assess the income-generation and profitability of real estate assets.

It is an important measure looked at by investors and creditors when evaluating properties for attractiveness and risk.

NOI is reported on the income statement and statement of cash flows and reports profitability before taking into account factors such as financing costs and taxes.

Along with analyzing profitability, the NOI metric is used for the valuation of a property’s worth using the “cap rate.”

To arrive at your NOI calculation, you would add up all forms of income from the asset and subtract all operating expenses related to the property itself.

A similar metric used in other industries is EBIT or Earnings Before Interest and Taxes.

If the calculation of net operating income ends up being negative, it is referred to as a “Net Operating Loss.”

NET OPERATING INCOME FORMULA

Here is the basic formula for Net Operating Income:

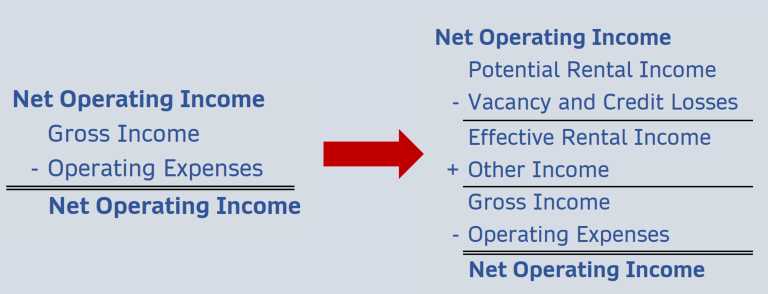

Net Operating Income = Gross Income – Operating Expenses

The formula can be further broken down into the formula below.

HOW TO CALCULATE NOI

Gross Income

First, we will need to determine the gross income amount for the asset.

To arrive at gross income we will take in all factors for:

- Potential Rental Income

- Vacancy and Credit Losses

- Other Income

Potential rental income is the sum of all rents that a property can produce. This is your ideal scenario when your property has 100% occupancy and everyone pays their bills on time.

It is best to start with this figure because it is the first item in the extended calculation of net operating income and it is the easiest amount to calculate.

Simply find out how much rent your property or properties will charge and sum that up.

Vacancy and Credit Losses

This line item is subtracted from potential rental income.

Vacancy refers to losses in income related to tenants vacating the property and the time period where no tenants are occupying.

If you know the property typically operates at a 90% occupancy, you could expect to receive 90% of your potential rental income amount.

If you charged rent for $1,000 a month at a 90% occupancy rate, you would realize $900 in rental income.

Credit losses refer to tenants defaulting on their rental payments and not paying them.

Like vacancy, a property probably operates with a certain rate of credit losses.

If credit losses were typically 5%, you would subtract that amount from you potential rental income.

Once those three items have been identified, subtract losses from vacancy and credit losses from your potential rental income to arrive at effective rental income.

Effective Rental Income

Effective rental income is your potential rental income amount less losses from vacancies and credit losses. This is the actual amount of rental income an investor could expect to earn from a property.

Other Income

The paragraphs above were related to calculating the expected rental income a property would produce from rents.

A real estate asset can also produce other forms of income not related to rent collections.

Some additional streams real estate properties can produce income from include:

- Parking structures

- On-site laundromat

- Vending machines

- Billboard/marketing space

- Locker/storage space

Whatever income a property produces unrelated to rent will be grouped into the “Other Income” line item.

Add your other income to your effective rental income to arrive at the gross income amount.

Operating Expenses

Next, we’ll move on to the other major part of the net operating income calculation: operating expenses.

Operating expenses are all expenses required for the day-to-day operation of the real estate asset itself.

It does not include costs for financing and taxes that are incurred by the owner or investor in a property. These costs do not relate to the income-generating potential of a property.

Examples of operating expenses include:

- Maintenance and repair

- Salaries and wages of staff

- Utilities

- Supplies

- Licenses

- Insurance

- Overhead costs

- Costs for professional services such as legal and accounting

- Property taxes (not income taxes that the owner/investor would incur)

Identify these expenses on a real estate asset and sum the amounts up to arrive at total operating expenses.

Subtract the total operating expenses from your gross income amount to finally arrive at net operating income.

ITEMS EXCLUDED FROM THE NOI CALCULATION

Now that you have walked through the calculation, let’s quickly walk through items that are not included in calculating net operating income and why.

Income Taxes

- Income taxes are specific to the owner or investor and do not relate to the performance of a property. Therefore, it isn’t included in calculating net operating income.

Debt Service

- Debt service is a financing cost that is also specific to the owner or investor and does not relate to the performance of a property.

Depreciation

- Depreciation is not included in the calculation because it is only an accounting method and not an actual outflow of cash.

Capital Expenditures

- Capital expenditures include major repairs, modification, and replacements and are typically irregular in frequency. Capex is not to be confused with standard maintenance and repairs that are included in operating expenses. They are not regular expenditures related to day-to-day operations of the property.

Tenant Improvements

- Tenant improvements are improvements made to a specific tenant’s rental space to fit the tenant’s needs. They are a form of capital expenditures and are not included in net operating income.

To make it easy, you can simply remember that all items included in the net operating income calculation are unique to the property itself and not the owner or investor.

WHAT NET OPERATING INCOME IS USED FOR

Net Operating Income is used by both investors and creditors.

Investors

Here is a quick bullet-list of how investors use NOI:

- Analyze profitability and size of cash flow

- Use in decision-making on a purchase or investment in a property

- Determine the ability to make debt payments

- Determine the valuation of a property

Creditors

Creditors use NOI for nearly all the same reasons as investors, except they look for the ability of their debts to be paid back to them by the income produced from a property.

A lender will not loan money to fund an investment in a property if it does not deem the borrower and property as creditworthy and likely to pay its debts.

Here is a bullet-list of how creditors use NOI:

- Analyze profitability and size of cash flow to determine a borrower’s ability to pay its debt payments

- Use in decision-making on whether to lend to an owner or investor or not

- Determine creditworthiness and the likelihood the NOI will be enough to make debt payments

- Determine the valuation of the property to gauge the size of a loan with minimized risk

VALUATION: NOI AND THE “CAP RATE”

One of the uses for net operating income is for the valuation of a property.

Using NOI and the cap rate can help you quickly determine a property’s relative valuation.

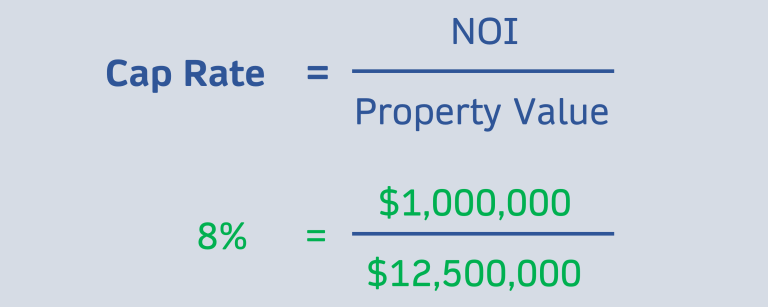

The capitalization rate, or cap rate, is a common ratio used in commercial real estate. The formula for cap rate is

Cap rate = NOI / Value (or purchase price)

Think of the cap rate as a percentage return an investor would need to receive on an all-cash purchase.

If your NOI is $1,000,000 and it sold or is worth $10,000,000 the cap rate would be 10%. If the property sold for $20,000,000, the cap rate would be 5%.

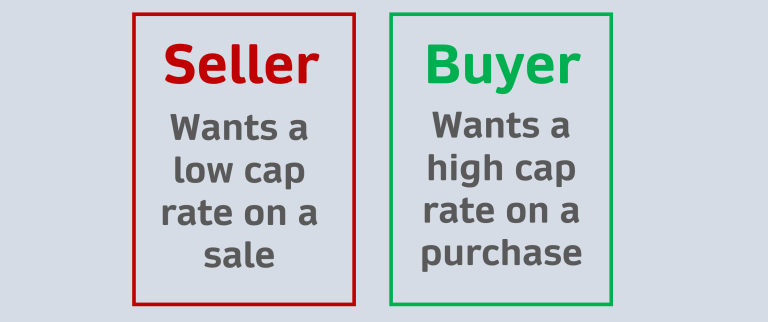

As a seller of a property, you want your cap rate to be lower because it would mean your property is worth a higher value.

If you are a buyer, you would want a higher cap rate because your investment would be lower for the amount of NOI you are receiving in a purchase of a property.

For valuation purposes, you can rearrange the cap rate formula to have…

Value of property = NOI / cap rate

In different industries and for different properties, there are average cap rates associated with each niche of properties.

You might be looking at the purchase of a shopping mall and know that shopping malls have been selling at a 8% cap rate for the past 18 months.

You could assume that you would be purchasing a shopping mall at around that rate.

If the mall you are looking at has a net operating income of $2 million per year, you could divide that by the 8% cap rate to arrive at a valuation of $25,000,000.

PROS OF NET OPERATING INCOME

- Gives investors an idea of the amount of profit they could expect from a property

- Helps determine the value of a property

- Helps investors determine their ability to pay their debts

- Helps lenders determine if a property has risk or not when lending

CONS OF NET OPERATING INCOME

- NOI can change when managed by one owner versus another

- NOI can be manipulated to look more attractive by accounting and the delaying of expenses

- Assumptions and estimations for rent, vacancies, credit losses, and operating expenses can lead to an inaccurate NOI and inaccurate valuation

SUMMARY

Net Operating Income is one of the most important metrics related to real estate properties.

It is essential to analyze the profitability of properties and determine their value.

It is simply calculated by subtracting operating expenses from gross income. Remember, operating expenses are expenses that relate to the day-to-day operations of the property.

Expenses related to the investor or owner are not included.

Like most financial formulas and metrics, there are pros and cons to NOI.

Keep them in mind when you need to calculate and make decisions based on NOI.

About Post Author

Brandon Hill

I'm Brandon Hill with Bizness Professionals. We serve content to help young professionals develop personally, professionally, and financially. Well-rounded improvement is a theme we live by. As such, this website will cover a variety of topics aimed to help you have a successful life and career.