This post may contain affiliate links, which means I’ll receive a commission if you purchase through my links, at no extra cost to you. Please read full disclosure for more information.

The statement of cash flows (or cash flow statement) is a financial statement produced by a company to provide information about its cash receipts and payments during an accounting period.

It is used to measure how well a company is managing its cash position and can be used to analyze a company’s liquidity, solvency and financial flexibility to pay bills, weather downturns, and pursue future business opportunities.

Cash inflows and outflows made are reported in the 3 ways a business receives and uses funds: operations, investments, and financing.

It is one of the 3 main financial statements a company produces, alongside the income statement and balance sheet. In fact, the statement of cash flows is constructed from the information presented on the income statement and balance sheet.

The statement of cash flows is preferred by many in the investment community for analyzing the true health and financial position of a company. This is due to the statement of cash flows being built on cash accounting, not accrual accounting like the income statement.

WHAT IS THE STATEMENT OF CASH FLOWS USED FOR?

The statement of cash flows is used for understanding the sources and uses of cash for a company, which can paint a picture of the financial health and position of a company and its future prospects.

With the structure of the cash flow statement, you can understand how cash is being generated or used on operations, investing, and financing.

It isn’t enough to just look at the ending cash flow number difference from period to period. The cash flows coming particularly from operations, investing or financing can tell you a lot about the state of a company.

This statement is used by management, investors, and creditors.

It is popularly looked at because it is thought to be the most transparent financial statement due to it being built on cash accounting principles.

With accrual accounting on the income statement, there is a lot that can be adjusted and misleading.

Differences between the statement of cash flows and income statement can stem from:

- Differences in timing between recognizing a transaction and actual cash received or spent

- Revenue recognition methods to report revenue or expenses in different time periods for an advantage

- Capex for assets requiring large capital investments are not shown on the income statement

The statement of cash flows is harder to manipulate, therefore showing the true cash health of a company.

You can use the statement of cash flows to determine if:

- The regular operations of the business can generate enough cash to sustain it

- Enough cash is generated to pay off debt obligations

- The firm will need financing

- The firm can weather a storm of unexpected obligations or a financial downturn

- The firm has the funds and financial flexibility to pursue attractive business opportunities when they present themselves

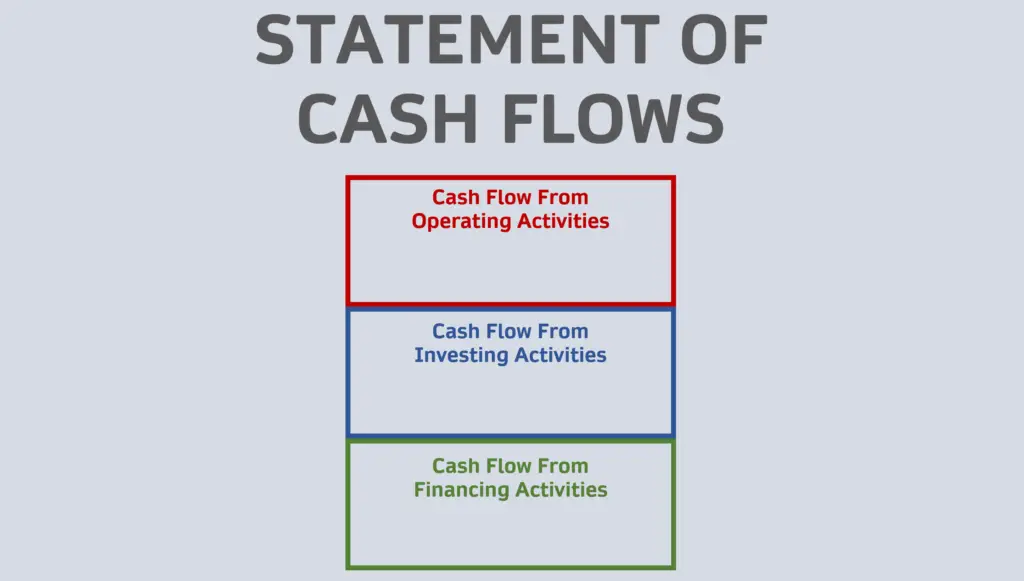

CASH FLOW STATEMENT STRUCTURE

The statement of cash flows is divided into 3 main parts:

- Cash from operating activities

- Cash from investing activities

- Cash from financing activities

Cash flow from operating activities

Cash flow from operating activities (also called cash flow from operations or operating cash flow) are the cash inflows and outflows resulting from transactions from the regular operations of a business.

This includes the cash sources and uses related to the business’s products and services.

Cash flow from investing activities

Cash flow from investing activities are the cash inflows and outflows resulting from the buying and selling of long-term assets and investments not considered cash equivalents.

Items found in this section can be property, plant, and equipment (PP&E), other non-current assets, and other financial assets.

This can include investing in other businesses and acquiring or divesting entire businesses.

This section is where changes in capital expenditures or (capex) can be found.

Capex increasing can be a good sign in the eyes of investors because it could indicate a company is making investments for its future. The returns on cash used to invest in new property could be greater than if that cash was used for something else.

Positive cash flow from investing activities isn’t necessarily a bad thing, but investors would rather see you generating cash flow from your normal business operations since that is the heart of your business.

A positive cash flow in this section would mean the company is selling its assets, which is fine for a one-time occurrence, but consistent selling of assets is not sustainable and can be a red flag on the company’s financial health.

Cash flow from financing activities

Cash flow from financing activities is the cash inflows and outflows resulting from transactions between a company, its owners and its creditors that affect its capital structure.

It is used to measure the cash flows through debt and equity.

Financing cash flows can include issuing shares, repurchasing shares, raising debt, paying off debt and paying dividends to shareholders.

These events all result in the changing of the size and composition of the company’s capital structure.

Cash flow from financing activities can help investors determine a company’s financial strength and if the capital structure is well-managed or not.

A positive or negative number for this section can be good or bad depending on the reason:

- A positive cash flow from financing could mean a firm isn’t generating sufficient earnings from operations

- Interest rates rising or declining can make borrowing or issuing debt attactive or non-attractive

- Repurchasing stock could mean a company has faith in itself and will expect the stock to rise

- Issuing dividends can show that a company is financially healthy. A cut in the dividend could be a warning sign

HOW TO PREPARE THE STATEMENT OF CASH FLOWS

The statement of cash flows is divided into 3 sections: operating activities, investing activities and financing activities.

Cash flows are built out for each section using items from the income statement and balance sheet.

For the first section, operating activities, the section can be shown through the direct or indirect method.

These two different methods are only used for the construction of the section for cash flow from operations.

Direct Method

For the direct method of constructing cash flows from operations, each line item from the income statement, which is based on accrual accounting, is converted to cash inflows and outflows.

The direct method basically turns the accrual-based income statement into a cash-based income statement.

The beginning and ending balances of the different accounts are adjusted to end up showing a net increase or net decrease in the account item.

Accounts include:

- Cash received from customers

- Cash paid for salaries and wages

- Cash paid to suppliers

- Income received from interest and dividends

- Cash paid towards interest and taxes

Notice how these accounts follow the layout of the income statement beginning with revenue, then operating expenses, then other income and finally cash outflows for taxes and interest.

This method is detailed and preferred for US GAAP and IFRS. However, most companies build their statement of cash flows using the indirect method.

Indirect Method

The direct method essentially takes net income and adjusts it to arrive at cash flow from operations.

Since net income comes from the income statement, which is built on accrual accounting, the indirect method will adjust net income for non-cash expenses (like depreciation and amortization) and non-operating items (gains and losses).

The indirect method also adjusts for changes in balance sheet account items including inventory, payables, receivables and liabilities

To summarize, accounts that are adjusted for with the indirect method include:

- Depreciation and amortization

- Gains or losses on sale of assets

- Changes in receivables and payables

- Changes in investory

- Accruals in liabilities

The direct method is great because of its detail on cash receipts and payments and the indirect method is great for reconciling the difference between net income and operating cash flow.

It is important to remind you that direct or indirect only applies to the section of the statement of cash flows on cash flows from operating activities.

Cash flow from investing activities and financing activities are constructed the same under either method.

Also note that both methods will arrive at the same amount for cash flow from operating activities.

HOW TO CLASSIFY TRANSACTIONS AS OPERATING, INVESTING OR FINANCING

When you are constructing the statement of cash flows you will be using transactions and items from the balance sheet and income statement.

Adjusting for cash inflows and outflows is simple, but can mix you up because it requires some inverse thinking.

Keep in mind that sources of cash are positive inflows and uses of cash are negative outflows.

The inverse thinking comes when you look at changes in assets and liabilities and changes in cash flows.

When there is an increase in an asset account, you might naturally associate an “increase” with “positive.”

You have to think the opposite with cash flow.

When your assets increase, you must have used cash to acquire the asset so it is a cash outflow.

When your asset account decreases, it must have come from a sale of an asset. A sale of an asset would bring a cash inflow.

It’s the same for liabilities.

When your liability account increases, it is a source of cash since cash was not used for the liability.

If a liability account decreases, it means the company paid down its liabilities, which is an outflow of cash.

Always ask yourself if something would require an inflow or outflow of cash.

Below are examples of cash inflows and outflows for all 3 sections of the cash flow statement.

Operating Activities

Inflows

- Cash received by customers

- Interest and dividends received

- Proceeds from trading securities

Outflows

- Cash paid for wages and salaries

- Cash paid for suppliers

- Cash used for goods and services

- Cash paid for other operating expenses

- Cash used to acquire trading securities

- Interest paid

- Taxes paid to government

Investing Activities

Inflows

- Proceeds from sale of PP&E, other long-term assets and intangible assets

- Proceeds from sale of equity and debt investments

- Collections of principal on loans made to others

Outflows

- Acquiring PP&A and other fixed assets

- Acquiring equity and debt investments

- Loaning funds to others

Investing Activities

Inflows

- Funds from issuing debt

- Funds from issuing equity

Outflows

- Principal paid on debt

- Funds used for stock repurchases

- Funds used for dividends paid for shareholders

HOW TO ANALYZE THE CASH FLOW STATEMENT

To analyze the statement of cash flows, you’ll look at the fundamentals of the sources and uses of cash for a company.

Just because cash flow is positive for an accounting period, that does not necessarily mean that everything is fine and well for a company financially.

You need to look deeper into the sections of the statement of cash flows and question and understand why items are positive or negative.

Positive and negative numbers for operations, financing and investing activities can be good or bad depending on the circumstance.

For a high-growth tech startup, several years of cash outflows from operating activities can be normal as the company focuses on growing.

Several years of cash outflows for a company in a mature industry can point to problems with the business.

Here are some tips for analyze the income statement:

Operating cash flow

- Identify if cash flow is generated by the company’s normal course of business. An increase in cash flow from operating activities due to something like unreasonable liquidation of inventory is not stable and shouldn’t be considered a good thing.

- Check net income versus operating cash flow. If the two are somewhat similar, the quality of earnings from the company are high. If the two differ by a large margin, the company may have used accounting rules to inflate their net income.

Investing cash flow

- Look at capital expenditures. Do they make sense? Would the investments lead to growth or would the expenditures lead to financial constraints if there was a recession?

- What is the company doing with the assets? Are they buying or selling? A positive cash flow from investing activities due to the selling of assets is fine for a one-time or occasional occurrence, but consistent selling of assets for cash flow is not sustainable and raises a red flag on health.

- Look for cash flow from operating activities to exceed capex

Financing cash flow

- Look at how much equity vs debt a company is raising. Is it appropriate? Is it efficient? Is it adding risk?

- Look for the company issuing and raising dividends. Investors like this and it could be a sign of good financial health

- See if the company is buying back its own shares. This can help its financial metrics, stock price and shows that a company is confident enough in its business for it to buy back its own stock.

Financial Ratios for Cash Flow

Financial ratios can help you in analyzing the performance and debt coverage of a company. Here are a few.

Note: CFO denotes cash flow from operations.

Performance

Cash flow to revenue

- CFO / Revenue

- Shows operating cash flow for every dollar of revenue

Cash return on assets ratio

- CFO / Average Total Assets

- Shows operating cash flow attributable to all providers of capital

Cash return on equity ratio

- CFO / Average total equity

- Measures return of operating cash flow attributable to all shareholders

Cash to income ratio

- CFO / operating income

- Measures the ability to generate cash flow from the firm’s operations

Cash flow per share

- (CFO – Preferred Dividends) / Avg Number of Common Shares

Coverage

Reinvestment ratio

- CFO / Cash Paid for Long-Term Assets

- Shows firm’s ability to acquire long-term assets with operating cash flow

Debt payment ratio

- CFO / Cash Long-Term Debt Repayment

- Shows ability for firm to satisfy long-term debt payments through operating cash flow

Dividend payment ratio

- CFO / Dividends Paid

- Shows ability for the firm to make dividend payments through operating cash flow

WHERE TO FIND CASH FLOW STATEMENTS FOR COMPANIES

If you have read my post on the income statement and balance sheet, you have seen where you can find financial statements for companies.

If you haven’t, here are some sources you can find the statement of cash flows and other filings from public companies:

EDGAR

- EDGAR stands for Electronic Data Gathering, Analysis, and Retrieval and it is a tool on the SEC website where you can find the filings of companies

- The link is to the EDGAR tool is here

Investor Relations Website

- On a company’s website, they will typically have an investor relations website with a bunch of information on the website they want their investors to know about, including financial statement filings.

- Here is a link to Hilton’s (HLT) Investor Relations website as an example

Sites like Yahoo! Finance

- Financial news websites like Yahoo! Finance will have interactive financial statements for public companies on their site. Simply search the company name or ticker in the search bar.

- As an example, here is a link to Tesla’s (TSLA) income statement

Bloomberg Terminal

- A Bloomberg Terminal is a computer software program that contains a massive amount of financial data on companies

- It is an extremely expensive subscription to have, but if you have access to one, you can find the SEC filings of a company on it

LIMITATIONS OF THE STATEMENT OF CASH FLOWS

Even though “cash is king” and the statement of cash flows is praised for the transparency it provides, it is not without its limitations.

Here are a few downsides to the statement of cash flows:

- Does not present net profitability because it does not take into account non-cash items like the income statement does

- Does not reveal liquidity and solvency

- Does not give the entire picture of the financial health and performance of a company alone. It needs to be considered along with the income statement and balance sheet

- Comparisons to other companies or industries require more than just knowing cash flows. The statement of cash flows doesn’t measure economic efficiency of a company, which is a way to compare one company versus another

Summary

In its simplest form, the statement of cash flows reports the cash receipts and payments of a company during an accounting period.

It is built from items from the income statement and balance sheet and is seen as transparent in reporting the cash a company is able to generate.

Check out our other posts on the income statement and balance sheet to get a full grasp on the 3 major financial statements.

About Post Author

Brandon Hill

I'm Brandon Hill with Bizness Professionals. We serve content to help young professionals develop personally, professionally, and financially. Well-rounded improvement is a theme we live by. As such, this website will cover a variety of topics aimed to help you have a successful life and career.