This post may contain affiliate links, which means I’ll receive a commission if you purchase through my links, at no extra cost to you. Please read full disclosure for more information.

A dilemma that many face in their personal finance life is whether they should use spare cash to invest or pay off debt. The books and articles we read tell us that both are beneficial, so which do we choose? What strategy do we implement?

I’ll share with you the thought process of going about this decision. Personally, I am constantly deciding whether I should invest or pay down debt.

By the way, this doesn’t have to be an all-or-nothing choice. You can invest and make debt payments at the same time. I usually do both and we will get into how later.

Deciding which one to do or how much of each to do will come down to three things:

- What payments must you make (ie minimum payments)

- The interest rate versus growth rate

- What emotional burden you can tolerate

INVEST OR PAY OFF DEBT? HOW TO DECIDE

The dilemma of this choice comes from the want of investing and the need of paying off debt. You want to invest because you know the investment has the potential to grow and set yourself up for retirement.

However, the need to pay down debt weighs on your ability to invest. You cannot simply ignore your debt payments and invest all your cash. Bills need to be paid or you’ll be shooting yourself in the foot with interest payments and a ruined credit score.

Follow these four steps to help you decide what route you’ll take.

1. First, Build Your Emergency Fund

Before using your money to invest or pay off debt, you should first build your emergency fund.

An emergency fund is a collection of savings that you build up to use as a financial safety net when inevitable emergency situations pop up. These financial emergencies may result from losing a job, a sudden illness, or major damage to any property or expensive belongings.

Use extra cash to build this first. You’ll always want to have a stash of liquid cash that could cover at least 6 months of your living expenses. If you spend $3,000 a month on rent, groceries, utilities, etc, you should have $18,000 saved up.

2. Make Mandatory Minimum Payments

So you have an extra $2,000 in cash at the end of the month. What do you do with it? You should look at the mandatory minimum payments you are obligated to pay for the month.

These can include payments on:

- Student loans

- Mortgage

- Credit cards

- Car loan

Each of these types of debt will have a mandatory minimum payment that needs to be made each month. Cover those payments first before deciding the further pay down your debt or invest.

3. Analyze Interest Rate vs Growth Rate

This will probably play the largest role in deciding how much you should allocate towards debt and investment. Basically, your interest rate on your debt will make your net worth decrease and the growth rate on your investment would make your net worth increase. It is simply a numbers game.

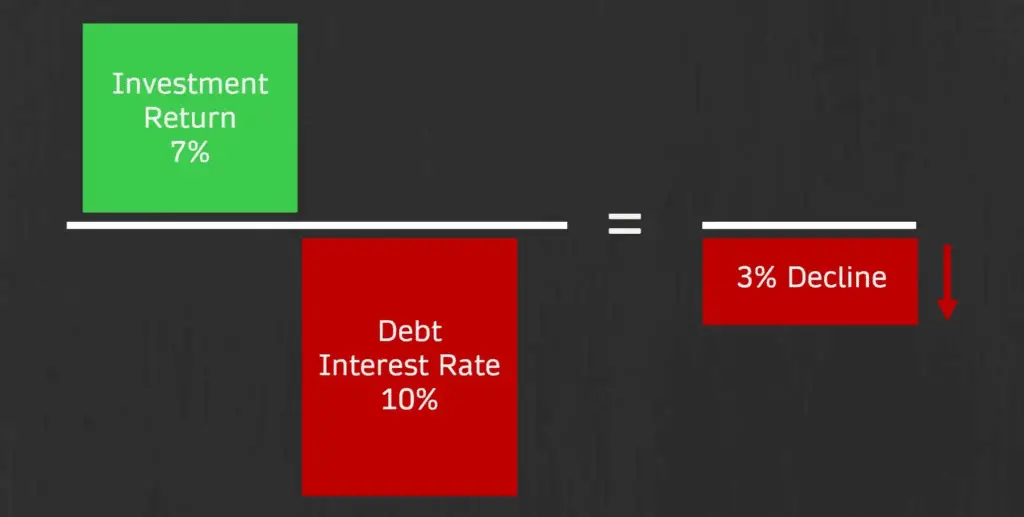

Assume these are after-tax rates. If your overall debt has an interest rate of 10% and your investment portfolio is expected to grow 7%, the net outcome of this is a 3% decline in net worth.

In this scenario, it wouldn’t make sense to use all your money to invest because the return does not exceed the interest rate on your debt. The debt is pulling you down more than your investment is lifting you up.

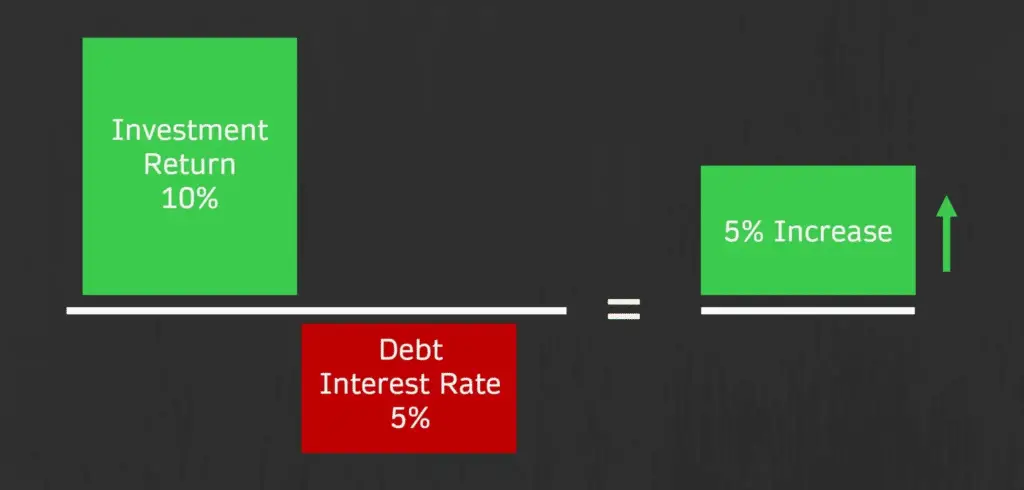

In another scenario, imagine the interest rate on your debt is 5% and you believe your investment will grow by 10%. Now, the net outcome is a positive 5%. In this scenario, it makes sense to invest since the rate exceeds the interest rate on the debt.

The art and the science

Okay, that all makes sense to you. Easy, right? Well, not exactly. While it’s easy to say your investment will grow by 10% each year, it is not a guarantee. Your investment could grow by 20% or could decline to $0.

Every investment is different and the market is mostly unpredictable in the short-term. This is where the art and science come into play. If you have faith in your investment abilities, you may achieve market-beating returns.

For the majority of the crowd, you can assume a 7-10% return since that is what the market has historically achieved over the long-term. This is over the long-term. Don’t rule out you experiencing a large drop in your investment’s value in the first few years.

Consider this when deciding between investing and paying off your debt. It’s painful to lose money on an investment when you could have used that money to get out of debt instead.

Pay down high-interest rate debt first

With interest rates and growth rates in mind, analyze your debt payments. If you have student loans, a mortgage, and credit cards, the credit cards will almost certainly have the highest interest rates with APRs of 20%+.

Strategize by paying down your credit card bills first since they are doing the most damage through their interest rates. When paying down debt, you will always want to pay down the high-interest rate debt first.

4. Consider the Emotional Burden Your Debt Causes

The numbers might make sense when you consider investing or paying off your debt. The net effect of investing may be positive, but the emotional effects of debt will need to be considered as well.

Does the thought of your debt raise your anxiety and stress levels?

Some people hate the feeling of owing money. It can be a lingering gray cloud above you. If this sounds like you, it may be more beneficial to use your extra cash to pay down your debt rather than invest it.

If paying down your debt will help you sleep at night, you should prioritize that. It wouldn’t be fun to invest money while still feeling anxious about the debt you owe. The returns from that investment are not worth the stress.

Everyone is different. Some want nothing to do with debt. For others, having debt does not bother them. Decide on what will be more beneficial to YOU. Weigh the benefits of earning a potential return on your investment versus the peace of mind of owing less debt or no debt.

MY THOUGHTS ON INVESTING VS DEBT PAYMENTS

For myself, my debts include my student loans and credit card debt. For the credit card debt, it is only the debt that has accumulated since the prior statement period. I do not allow my credit card balances to pile up month after month.

My decision making for investing or paying down debt is as follows:

- Make all minimum monthly debt payments

- Pay down high-interest debt like credit cards

- Invest only after 1 and 2 have been done

Simply put, I make my monthly payments, pay down my high-interest rate debt, and THEN invest after.

Investing instead of paying down student loans

I do have a hefty amount of student loans, but I choose to invest my extra cash rather than accelerate the paying down of my student loans.

I have confidence in my ability to grow my money at a higher rate than my student loan interest rates. If my student loan interest rates hover around 5%, I’ll look at any potential investment and ask myself if I can earn more than 5%. If I believe I can, I’ll make the investment.

WAYS TO SAVE MONEY TO INVEST OR PAY OFF DEBT

Before you can invest or pay off your debt, you will need to save money first. Saving can be difficult because it is easy to spend the extra cash in your account when you see it available.

I prefer to automate my savings, and it is recommended in two personal finance books I have reviewed: Financial Freedom and I Will Teach You To Be Rich.

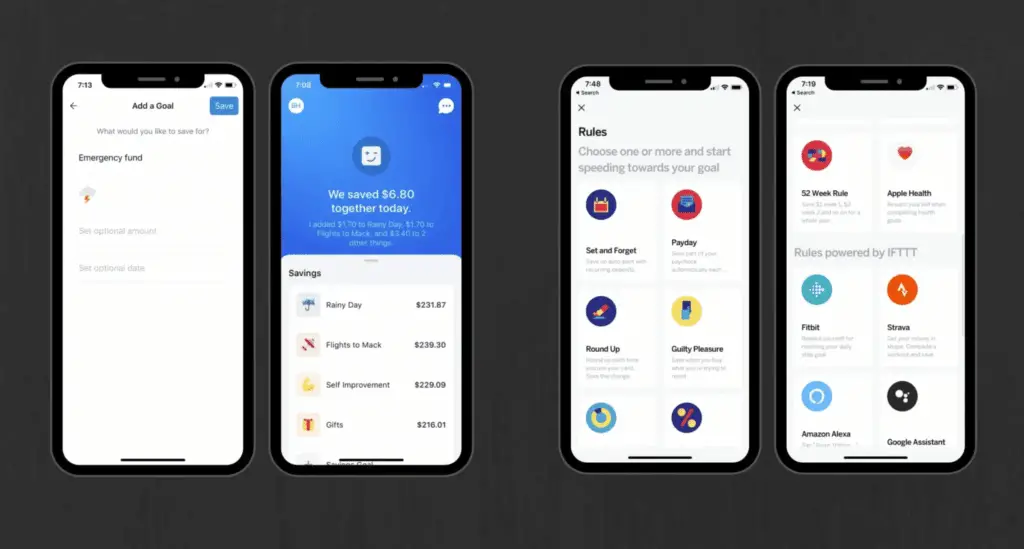

I utilize two mobile apps to help me save:

- Digit (Sign up here and we’ll both get $5!)

- Qapital (Sign up here and we’ll both get $5!)

If you only want to use one app, I would use Qapital. While both apps initiate the process of you saving money, they do so in different ways. That’s why I use both.

Digit analyzes your spending habits and automatically withdraws the optimal amount. Qapital allows you to set up savings accounts using a variety of rules that make saving more fun. Both offer ways to automate your savings by withdrawing funds from your checking account on autopilot.

Check out this post too: Importance of Saving Early in Your Career

SUMMARY

It’s nice to have extra cash lying around, but what do you do with it? Do you invest it or pay off your debt?

Both are responsible moves and this is a common dilemma people run into. After your mandatory bills have been paid, it will come down to 1) the interest rate vs growth rate and 2) the emotional burden you are willing to tolerate.

About Post Author

Brandon Hill

I'm Brandon Hill with Bizness Professionals. We serve content to help young professionals develop personally, professionally, and financially. Well-rounded improvement is a theme we live by. As such, this website will cover a variety of topics aimed to help you have a successful life and career.