This post may contain affiliate links, which means I’ll receive a commission if you purchase through my links, at no extra cost to you. Please read full disclosure for more information.

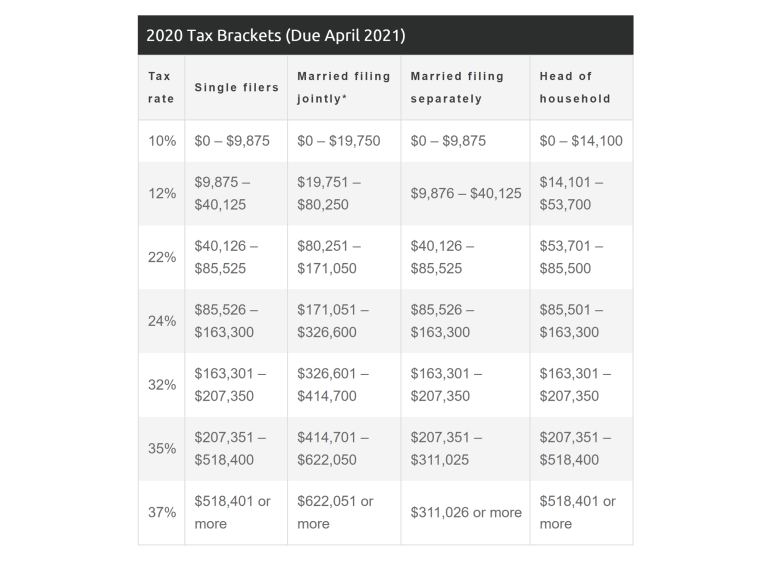

TAX BRACKETS AND THE US PROGRESSIVE TAX SYSTEM

The United States uses a progressive tax system, meaning that different portions of taxable income are taxed at different rates, with those rates increasing as the taxable income level increases.

To put it simply, people with higher income levels end up getting taxed at higher federal income tax rates.

The federal tax system divides tax rates into 7 tiers called tax brackets.

Each tax bracket is related to a certain range of taxable income and each tier has an associated tax percentage rate.

The 7 tax rates for the 2020 tax brackets are 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

These 7 levels of tax rates are applied to different levels of income, with higher income levels taxed at the higher tax rates. The income ranges for each tax rate level can differ based on your filing status.

You can file as single, married and filing jointly, married and filing separately, and head of household. These filing differences result in higher amounts of income being taxed at a lower tax rate for certain filing statuses.

See the table below sources from debt.org for the taxable income ranges for each of the 4 statuses for filing.

COMMON CONFUSION ON HOW TAX BRACKETS WORK

Tax brackets can be confusing and are often misinterpreted.

The first way tax brackets are misinterpreted is with salary levels being compared to the income ranges of the tax brackets.

Some people look at the tax bracket income levels and use their salary number to classify themselves into one bracket or another.

An individual might make $42,000 a year for a salary and think they fall into the 22% tax bracket.

This is incorrect.

The income amounts you see on the tax bracket tables are for taxable income. Your salary is part of your gross income.

Taxable income is the portion of gross income that is actually subject to being taxed. Taxable income is calculated by taking your gross income amount and subtracting any tax deductions and exemptions you may qualify for.

With these deductions and exemptions, taxable income is always smaller than your gross income amount.

If an individual made $42,000 a year, it is very likely their taxable income amount will be under the $40,126 cutoff, which would put them in the 12% tax bracket.

The income amounts on the tax brackets are not to be directly compared to your salary. Your full salary is not your taxable income amount.

Another area of confusion with tax brackets is with the amount and rate an individual’s taxable income is taxed at.

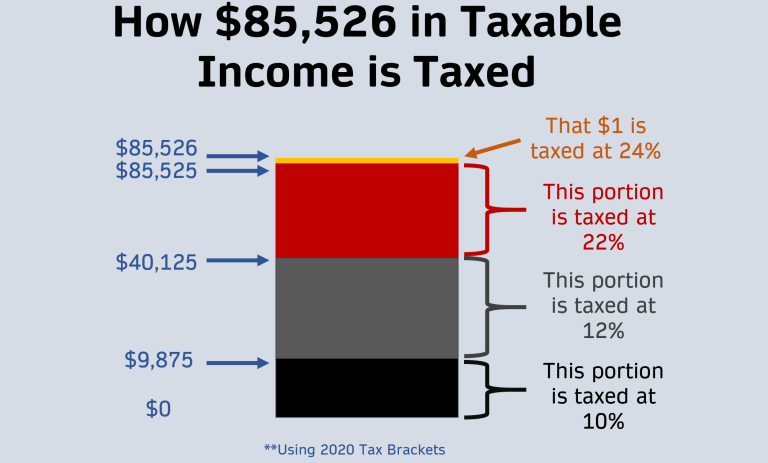

For example, let’s say someone files as single and has a taxable income amount of $85,525, which is right at the top of the 22% tax bracket level. That person would pay $18,816 in taxes and would take home $66,709.

Some people out there think that making $85,526 would be detrimental to their take-home pay because that would bump them into the 24% tax bracket.

They think that would lead to them paying $20,526 in taxes and taking home $65,000, which is less than the amount when they were in the 22% tax bracket.

This is not how the US federal tax system works and this is incorrect.

Each tax rate only applies to the income within a specific tax bracket. If you earn $1 more dollar taking you from $85,525 to $85,526, only that additional $1 would be taxed at the 24% level.

Your entire income is not taxed at the 24% level. Being in a tax bracket doesn’t mean that you pay that specific rate on all income you earned.

Let’s take a look at the screenshot below for someone filing as single.

For whichever tax bracket you fall into, you do not pay the tax rate of that bracket on your entire taxable income amount, only a portion of it.

EFFECTIVE TAX RATE

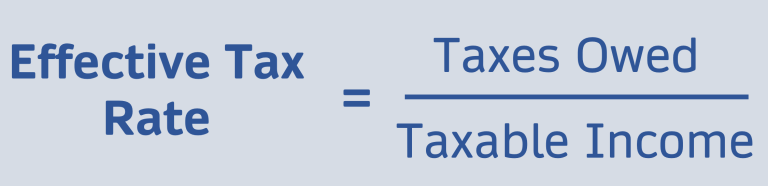

The effective tax rate is the rate of taxes that an individual actually ends up paying to the IRS.

The tax rate you pay for your highest chunk of income is likely a lot higher than the overall average tax rate you end up paying.

To calculate your effective tax rate, take the amount of taxes you owe and divide that by your taxable income amount.

If you owe $15,000 in taxes and your taxable income is $80,000, your effective tax rate is around 19%.

Even though a taxable income amount of $80,000 puts you in the 22% tax bracket, you only ended up paying at a 19% rate.

HOW TO GET INTO A LOWER TAX BRACKET

It is possible for you to jump down into a lower tax bracket through tax deductions.

A tax deduction is a deduction that lowers one’s taxable income amount, which therefore lowers the amount of taxes owed.

If your taxable income amount is $50,000 for the year and you qualify for a $5,000 tax deduction, your taxable income would reduce to $45,000 and only the $45,000 would be subject to tax.

Examples of common tax deductions include:

- Standard deduction

- Sales tax deduction

- Charitable contribution deduction

- Student loan interest deduction

- IRA contribution deductions

- Mortgage interest deductions

Tax deductions aren’t always advertised in plain sight. By taking extra time and effort to see what you qualify for, you can find tax deductions to take to reduce your taxable income amount.

ANOTHER WAY TO REDUCE THE AMOUNT OF TAXES YOU PAY

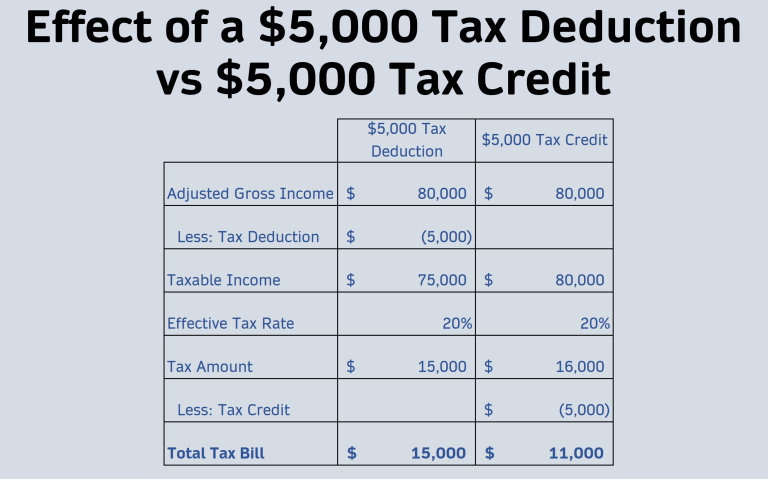

While this won’t help you jump down to a lower tax bracket, another way to reduce the amount of taxes you pay is through tax credits.

A tax credit is a dollar-for-dollar credit to reduce your tax bill. It differs from a tax deduction because a tax deduction only reduced your taxable income amount.

A tax credit actually reduces the taxes you pay on a dollar-for-dollar basis.

Examples of tax credits include:

- American Opportunity tax credit

- Lifetime Learning tax credit

- Residential Energy tax credit

- Low Income Housing tax credit

- Savers tax credit

Since tax credits directly reduce your taxes owed and tax deductions just reduce your taxable income amount, tax credits are more attractive when looking at a tax deduction and tax credit of equal amounts.

Look at the example below to see the effects of a $5,000 tax deduction vs a $5,000 tax credit.

SUMMARY

Understanding tax brackets and the US progressive tax system is important for personal finance.

It allows you to determine how much you’ll owe in taxes.

It is important to understand that the income levels for tax brackets are for taxable income amounts and the tax rate you fall into is not the rate your entire taxable income amount is taxed at.

To reduce the amount of taxes you pay, you can use tax deductions and tax credits. A little research to find out what you qualify for can go a long way and save you money in taxes you don’t have to pay.

About Post Author

Brandon Hill

I'm Brandon Hill with Bizness Professionals. We serve content to help young professionals develop personally, professionally, and financially. Well-rounded improvement is a theme we live by. As such, this website will cover a variety of topics aimed to help you have a successful life and career.