This post may contain affiliate links, which means I’ll receive a commission if you purchase through my links, at no extra cost to you. Please read full disclosure for more information.

Depreciation is an accounting method used to allocate the cost of a tangible asset over the course of its lifespan. Assets subject to depreciation have a lifespan (or useful life in accounting language) greater than one year. Examples include:

- Machinery

- Buildings

- Furniture

Depreciation expense reduces an asset’s book value with each passing year. This reduction represents the asset’s decline in value due to use, wear and tear, and obsolescence.

As a company, if you were not able to allocate the cost of an asset over time, you would have to recognize the entire expense in the year you bought it. Your income statement and profits would take a major hit. With depreciation, the cost of the asset is recognized on the income statement over time.

Matching Principle

This adheres to the matching principle, which is an accrual accounting principle that requires revenues earned in an accounting period to be matched with related expenses.

An asset such as a new office building will earn revenue for a few decades. Therefore, an expense like depreciation will be matched and recognized for a few decades.

Depreciation can be calculated in several ways. The different methods provide options for selecting the most appropriate method for an asset type. We will dive into the different ways to calculate depreciation later in the post.

DEPRECIATION GLOSSARY

To help you in understanding the opening section and the subsequent sections of this post, here is a glossary of terms related to depreciation to refer back to.

Useful life – How long an asset can be used for

Salvage value – Value of an asset after all depreciation has been deducted

Book value – The value of an asset on a company’s “books.” This refers to their accounting books and balance sheet

Accumulated depreciation – The accumulation, or sum, of all depreciation recorded against an asset at a point in time

Carrying value – The value of an asset at any given time calculated by taking the historical cost minus accumulated depreciation

Depreciation expense – The amount of depreciation to be recognized in one accounting period

Tangible asset – Assets that have a physical form such as equipment, land, and inventory.

Matching principle – An accrual accounting principle that requires revenues earned in an accounting period to be matched with related expenses

RECORDING AND ACCOUNTING FOR DEPRECIATION

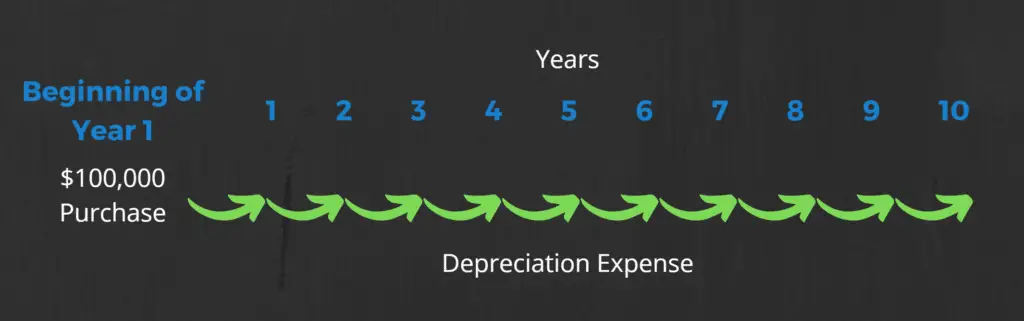

If an asset is purchased for $100,000, that entire amount is spent up front. The expense for that purchase is recorded incrementally over time through depreciation. Instead of recognizing the entire expense in the year the purchase was made, the expense is recognized over the course of the asset’s useful life.

This follows the matching principle in accounting so the expense matches the time period the asset provided benefit.

Think about it. If you spent $100,000 on an asset, with a useful life of 10 years, it would not make sense to recognize $100,000 in expense in year 1. You would still have 9 more years of useful life after that. Instead, it makes sense to recognize that expense over the 10 years.

Financial Statements

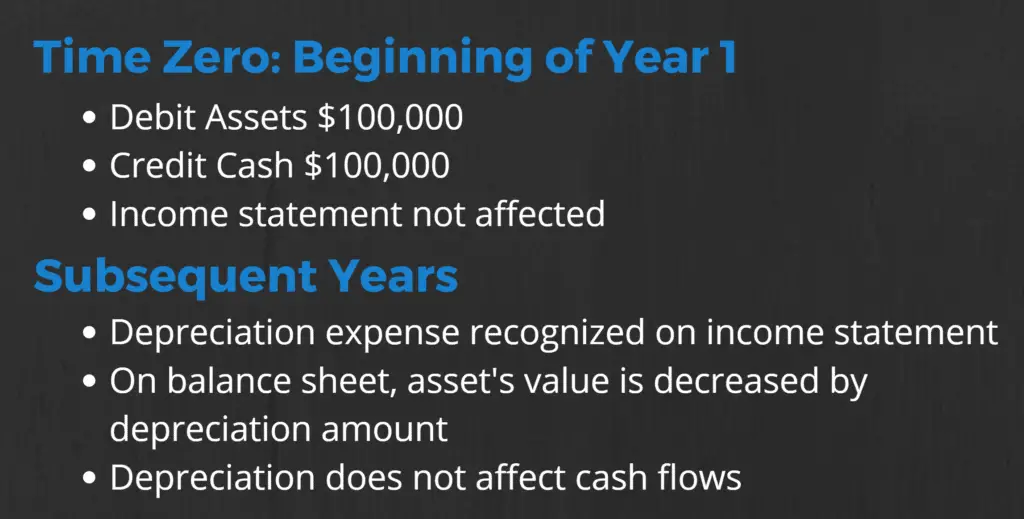

At the time of the purchase, the asset side of the balance sheet will be debited for $100,000 and cash will be credited $100,000. The income statement is not affected at the start.

Each year, your business’s income statement would recognize “depreciation expense.” In the case of a $100,000 asset with a useful life of 10 years (and a salvage value of zero), depreciation expense would be $10,000 per year (if using straight-line depreciation).

On the balance sheet, your asset’s book value would decrease by the amount of depreciation. For example, after year one, your asset on your balance sheet would decrease from $100,000 to $90,000. At the end of year two, it would be $80,000 and so forth until the value reaches zero.

It is important to remind you that depreciation is a non-cash expense. It is simply an accounting method and cash is not involved when depreciation expense is charged.

As a result, depreciation is added back on the statement of cash flows since it is a non-cash expense. Depreciation expense does not affect cash flow, but it does decrease a company’s earnings still.

Tax Purposes

For tax purposes, the IRS publishes depreciation schedules that list various types of assets and provide detail on the number of years certain assets can be depreciated.

For example, some machinery on the schedule are allowed 10 years for depreciation. Tools are depreciated 4 years. The years follow the expected useful life of each asset. The point is to try to accurately match expenses with the years assets are providing value.

TYPES OF DEPRECIATION – WITH EXAMPLES AND CALCULATIONS

Straight-Line Depreciation

Straight-line is the most common method of calculating depreciation due to its simplicity. Through straight-line depreciation, an equal amount of depreciation is deducted each accounting period over the course of an asset’s useful life.

The first step is to calculate the depreciation expense. The variables to the equation are cost, salvage value, and useful life.

- Depreciation Expense = (Cost – Salvage Value) / Useful Life

- Straight-line rate = 1 / Useful Life = 1/5 years = 20%

In this example, our cost is $100,000, the salvage value is $0, and the asset has a useful life of 10%.

Once depreciation expense has been calculated, you can set up a depreciation schedule as seen in the screenshot below. As you can see, the depreciation expense is fixed at $10,000 per year. In the chart on the right, you can see the “straight line.”

Each year, depreciation expense is subtracted from book value until the end of year 10, when the book value of the asset reaches its salvage value of $0.

While this method is simple, its simplicity can be a drawback since an asset’s actually depreciation in value may not follow a straight line.

Double-Declining Balance (DBB) Depreciation

DDB is an accelerated depreciated method, with the highest depreciation expense taken in the first year. Each year, the depreciation expense will decline.

Double-declining balance could make sense to use because an asset’s most productive years are at the start. Over time, the asset is less productive. Therefore, depreciation should be highest in the earlier years.

In this example, cost will be $100,000 and salvage value will be $10,000 this time. Another variable exclusive to this method is the rate the depreciation will be deducted. This is the double-declining balance rate, or DDB rate. To calculate the DDB rate, use the equation:

- DDB Rate = (1 / Useful Life) x 2

The “double” in the name comes from the multiplier of 2 in the equation. In the screenshot below in cell C7, the DDB rate for this example is 20%. That 20% rate will be applied to book value each year to calculate the depreciation expense.

- Depreciation Expense = DDB Rate x Beginning Book Value

In the table, you can see how the 20% rate is multiplied by the beginning book value of the year. In column E, it is clear that the highest depreciation expense is taken at the end of year 1 and the expense declines each year. A visual representation of the decline is seen in the chart.

In year 11, only $737 in depreciation is deducted to arrive at the $10,000 salvage value of the asset.

Units of Production Depreciation

For the units of production method, there is an equal amount of depreciation expense for each unit produced or hour of service rendered by the asset.

This method’s benefit is that depreciation is matched according to output by the asset. In a year where an asset produced more units of product, it would make sense to allocate more depreciation in that year compared to another year where the asset produced half as many units.

The main variable to find here is the depreciation cost per unit. This is the amount of depreciation that will be deducted for each unit an asset produces or each hour the asset provides service. Calculate it with the equation below:

- Depreciation Cost Per Unit = (Cost – Salvage Value) / Expected Usage of the Asset

In this example, the machine has an estimated usage of 60,000 hours. Using the equation, depreciation cost per unit will equal $1.50. For every hour, $1.50 of depreciation expense will be charged. Depreciation expense is calculated with this formula:

- Units of Production Depreciation Expense = Depreciation Cost Per Unit x Actual Usage of the Asset

In the table, column D shows the hours of usage for each year. In column C, the depreciation cost per unit is shown. Multiply the two to arrive at each year’s depreciation expense in column E.

Subtract that from book value each year until you arrive at the salvage value of $10,000. In the chart, you can see the line is volatile year to year based on the hours the machine was used. In years where the machine had more use, a higher amount of depreciation was deducted.

DEPRECIATION VS AMORTIZATION VS DEPLETION

Depreciation, amortization, and depletion are often confused to be the same thing. They are related in that they are accounting methods used to expense the value of assets/resources over time. Also, all three are non-cash expenses. Let’s discuss how they differ.

Depreciation – As mentioned, depreciation allocates the cost of a tangible/physical asset over the course of its useful life. Each year, a portion of its historical cost is deducted from the asset’s value through a depreciation expense.

Amortization – Amortization is similar to depreciation, but applies to intangible assets such as trademarks, patents, copyrights, etc.

Depletion – Depletion is common in industries including mining, oil, and timber. With depletion, a decline in value is allocated over time to represent the depletion or reduction of reserves the asset (site of mining, oil well, land with trees) has left. Reserves gradually exhausting over time can be compared to assets losing value to wear and tear over time with depreciation.

Just remember:

- Depreciation is for tangible assets

- Amortization is for intangible assets

- Depletion is for assets with limited resources

WHICH ASSETS DO NOT DEPRECIATE?

Not all physical assets are depreciated. Land is not depreciated since it is assumed to have an unlimited useful life. Land does not depreciate in value over time. In fact, it appreciates.

Nearly all other fixed assets have a useful life. A company car will stop running. Buildings will break down from wear and tear. Equipment will become obsolete.

However, land will always be useful for one way or another.

PROS AND CONS OF DEPRECIATION

Pros

- The cost of an asset is not recognized upon purchase. It is recognized over time

- Depreciation expense allows for a tax deduction

- Asset’s book values are more accurately reflected on balance sheet

Cons

- The useful life or usage for assets may not always accurately represent its decline in value

- The chosen depreciation method of choice may not be optimal

SUMMARY

Depreciation is simply an accounting method used to allocate the cost of a capital asset over time.

With the matching principle, expenses are to be matched with the time periods that an asset provided a benefit.

This is beneficial to companies. If they were not able to depreciate their assets, their income statements would take a huge hit by recognizing the entire expense in the first year. Another benefit of depreciation is that it is tax-deductible, allowing individuals and companies to lower their taxable income.

There are several methods used to calculate depreciation. The goal is to use the method that is most appropriate for the asset.

About Post Author

Brandon Hill

I'm Brandon Hill with Bizness Professionals. We serve content to help young professionals develop personally, professionally, and financially. Well-rounded improvement is a theme we live by. As such, this website will cover a variety of topics aimed to help you have a successful life and career.