This post may contain affiliate links, which means I’ll receive a commission if you purchase through my links, at no extra cost to you. Please read full disclosure for more information.

Note: This article is for informational use only and you should consult with a professional before making a decision.

WHAT IS A TARGET DATE FUND?

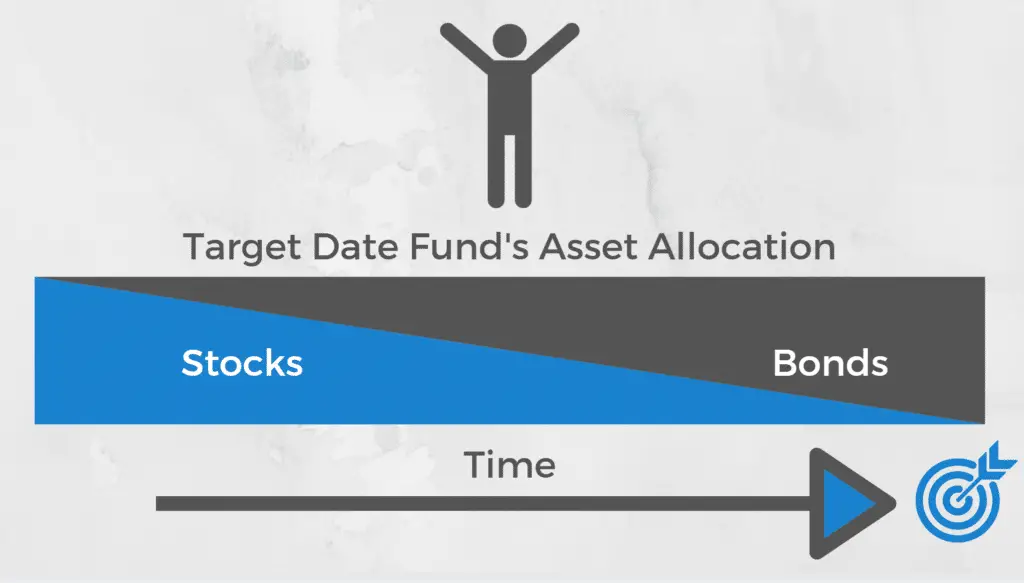

A target date fund (also called “lifecycle fund” or “TDF”) is an investment fund comprised of multiple asset classes and is managed to rebalance its weight in those asset classes over a long time horizon. It initially starts off in a more aggressive approach and moves towards a conservative approach.

They are simple, versatile, and effective options for investment in a retirement account.

The name “target date” derives from the characteristic that you choose a fund with the specific date you intend to retire. For example, you can choose funds that will have “Target Retirement 2065” or “Target Retirement 2060” in the name of the fund.

This means that fund is designed for their investors to retire at those dates and the asset allocation will be balanced accordingly.

When you are a young saver/investor and far from your target date, the fund will be heavy in stocks. As you age and approach your retirement and target date, the fund will end up being heavier in bonds and safe assets to preserve your nest egg.

This gradual shift towards conservative asset allocation is called the fund’s “glide path.”

Since target date funds automatically rebalance asset classes over time according to their glide path, they are popular for their simplicity and convenience. An investor’s investing activity is set to autopilot essentially. It is a “set it and forget it” approach.

The headache and guesswork of choosing the right investments and appropriate asset allocation is left to the manager of the target date fund

All the investor has to do is keep contributing towards the fund. This makes is easy to save and invest for retirement and the investor gets the benefit of diversification and asset allocation, the two elements that determine the performance of a portfolio.

Theoretically, an investor could simply use a target date fund as the only investment vehicle he or she uses for retirement. Even though it is a single fund, it offers everything an investor needs

Since target date funds are seen as all someone would need, they are often the default investment choice for 401(k) and Roth 401(k) plans. You will have to check with your employer to see if this is the case for you. You may already be invested in a target date fund if so.

Target Date Fund Structure

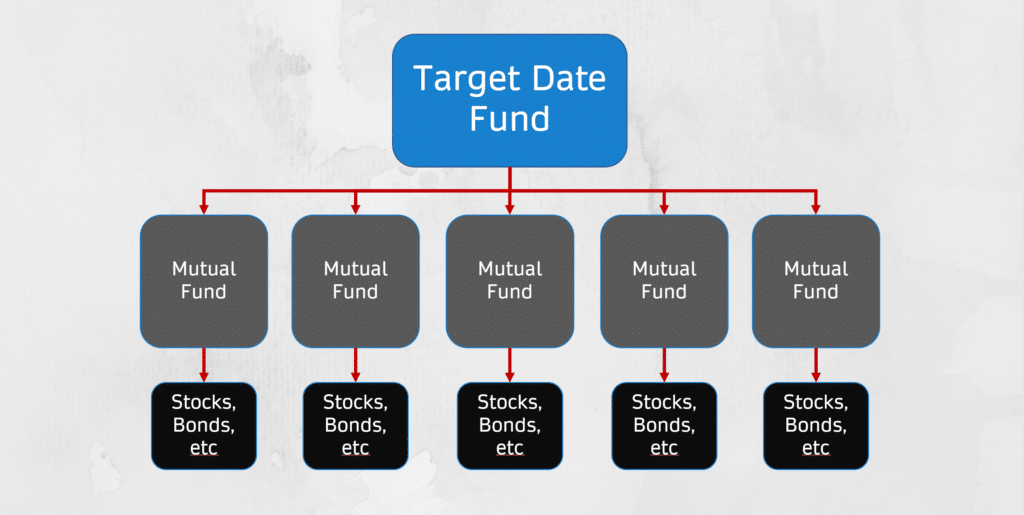

A target date fund is in the class of mutual funds and is usually structured as a “fund of funds.”

This means that the target date fund will be comprised of holdings in other funds, such as mutual funds, instead of holding individual securities. The mutual funds they own will hold the securities of stocks, bonds, and other asset classes.

By doing this, the fund is able to achieve its target asset allocation at any time. Additionally, the fund of funds structure offers broad diversification.

Imagine that a target date fund has holdings in 5 mutual funds, each with separate focuses on asset classes and strategy. Each of those mutual funds has 100 holdings. That would mean the target date fund actually had exposure to 500 holdings, even though its money is allocated to only 5 mutual funds.

TYPES OF TARGET DATE FUNDS

Target funds can vary on several characteristics:

Risk – Funds may lean towards low, moderate, or high risk portfolios.

Goals – Funds can be goal specific. For example, a target date fund may aim for growth, balance, or to produce income.

Composition – The composition of a target date fund can be built with different mutual funds and those mutual funds each hold a variety of securities. Target date funds can hold US, global, and emerging market securities. Equities can be small, mid, and large-cap companies.

Management – These funds can vary on how active or passively managed they are

These 4 characteristics can lead to large differences between one fund and another.

If you decide a target date fund is the route you want to go, just remember that not all of them are the same.

EXAMPLES OF ACTUAL FUNDS

Here are a few examples of actual target date funds that could be useful for those currently 20-30 years old

- Vanguard Target Retirement 2060 Fund (VTTSX)

- Vanguard Target Retirement 2055 Fund (VFFVX)

- Fidelity Freedom 2050 Fund (FFFHX)

- T. Rowe Price Retirement 2060 Fund (TRRLX)

BENEFITS OF TARGET DATE FUNDS

One-stop-shop investment vehicle

Target date funds offer a one-stop shop investment vehicle option. You could use a single fund to house your retirement investments and you would have diversification and proper asset allocation on your side.

This makes saving and investing much less cumbersome which is beneficial to investors that are not as sophisticated or don’t have time to learn how to invest on their own

Potential for low fees and tax advantages

Depending on the fund provider you go with, target date funds can have low expense ratios, meaning that the fund charges minimal fees.

Fees, even if only 1% or 2% per year, will eat into a large chunk of your earnings over the course of your career. You want to put your money into funds that have the lowest fees possible. Many mutual funds have expense ratios upwards of 1%-3%.

Many Vanguard target date funds have expense ratios under 0.3%.

In addition to the fees, target date funds can be tax advantaged. You can realize the tax benefits through mediums such as your 401(k) account. This is superior to investing in a mutual fund on your own through an account that does not have tax advantages.

“Set it and forget it” way to invest

Target date funds are popular for their convenience. It truly is a “set it and forget it” investment vehicle. Once enrolled, all you have to do is keep funding your investment accounts and wait until retirement.

Everything else is done for you and you don’t have to think about anything or lift a finger. Simply monitor your account every now and then.

Professionally managed investments

Target date funds are managed professionally by fund managers. The fund manager and their team will manage the fund adhering to the fund’s investment style and goals.

The odds of an individual investor outperforming the market year over year over the course of a 40-year investment career are abysmal. Even if you opt to invest in index funds, you will still have to choose which funds to invest in and how much to invest in each fund to achieve your target asset allocation.

With target date funds, this is all done by professionals

Offers a diversified portfolio

Target date funds are usually comprised of holding in other mutual funds. This fund of funds structure offers an investor a broad diversification of holdings.

The management team will make sure their fund is properly diversified and not overly exposed in any one type of asset.

Asset allocation is automatically optimized

Even more important than diversification, target date funds offer asset allocation and it is automatically adjusted over time.

Research has shown that asset allocation is said to determine over 90% of the variation in a portfolios return over time. It is an art and a science that is hard to do on your own. Target date funds managing your asset allocation until your target date is the best feature of this product in my opinion.

DRAWBACKS OF TARGET DATE FUNDS

One size fits most, but not all

Target funds are seen as a “one size fits all” investment fund, but actually, its more accurate to say “one size fits most.” You may find that none of the target date options exactly fit what you are looking for.

You’ll have to dig through to find a fund that offers the style you want, date you want to retire, low fees, and aligns with your goals.

Some investors will find funds that meet all their requirements, but some may never find the perfect fund. If that’s the case, the better option could be to choose another route, like index funds. It may be a better option, but it won’t be the easier option.

You will have to balance how picky you want to be with how much effort you want to put in

Autopilot can work against you

Autopilot is a great characteristic of the target date fund. Although it can benefit you as an investor, it can also work against you.

These funds automatically rebalance asset classes over time and move towards a conservative portfolio. This will work against you if you are still somewhat young and far from retiring and your fund begins taking risk off the table.

Yes, your portfolio will be conservative, but you will be cutting off potential growth your funds could be earning if the portfolio remained less conservative.

The returns on stocks are higher than the returns on bonds. A target date fund can cap off growth over time as it moves towards less risky assets. You will have to weigh this in your decision making. You can get around this by choosing a target date fund that specifically aligns with your risk tolerance.

Can be expensive depending on choice

Target date funds provided by places like Vanguard have low expense ratios, but there are funds out there that can get expensive. Do your research and compare the fees of one fund versus another.

Even a few tenths of percentage points can have substantial effects on your earnings over time

Not all funds are created equal

Not all target date funds are created equal.

They can differ by the date itself and through its investment style and characteristics. You, as the investor, will have to do some due diligence on the fund you are considering investing in.

Don’t just throw your money at the first target date option you see. While 10 funds may all fall under the category of target date funds, they can all be managed in different ways and charge different fees.

Underlying funds can be owned by the same company

We mentioned how you can theoretically use one target date fund as the single investment vehicle for your retirement. This works in theory, but may not be practical.

One downside of investing in a target date fund is that the funds it holds might also originate from the same fund provider.

For example, a Vanguard target date fund will hold Vanguard mutual funds within it. Many of these providers have flawless reputations and are considered safe, but anything can happen. You might not feel comfortable having all your funds managed by one company.

Even though your money is diversified in how it is invested, it is not diversified with who is holding and investing that money.

Potential for losses. Gains aren’t guaranteed

Finally, a target date fund is not a fund that is guaranteed to preserve your investments and produce income for you. It is an investment fund and has the potential for losses. It’s commonly mistaken that a target date fund can only go up. This is false and there is risk involved with investing.

Investors should be aware of this, but also realize markets historically go up over time. If your portfolio took a hit in one year, it is likely the fund will recoup its losses and trend upwards.

IS IT A GOOD INVESTMENT OPTION FOR ME?

After reading the benefits and drawbacks, you may be wondering if a target date fund is a good investment option for you.

That will depend on a few things:

- What is your retirement timeline?

- How long do you think you will live?

- Have you carefully thought about your target date?

- How much risk are you willing to take?

- Are you comfortable with the fund’s automatic rebalancing over time?

- Do you want your investments on autopilot or do you want to be more hands on?

Answers to these questions will help you determine if a target date fund is the option for you or if you should go another route.

Understand that there are many options for investing for your retirement. Some may require more research and effort from you, but there are options out there where you can produce the same diversification and asset allocation attributes that target date fund offers.

The degree of both can be within your control.

HOW TO ENROLL OR SIGN UP FOR A TARGET DATE FUND

There are three ways to enroll and sign up for a target date fund:

- Target date funds are popular options for employer-sponsored retirement plans such as the 401(k). If your employer offers a 401(k) and gives the option to invest in a target date fund, you can enroll.

- Another way to shop for a target date fund is to open up a brokerage account and search the options they offer.

- The third way is to open an account with target date fund providers such as Vanguard, T.Rowe Price, and Fidelity. Usually when you go through the target date fund providers, options are more limited because you will only be offered fund options from the individual provider. For example, if you sign up with Vanguard, your target date fund options will likely all be Vanguard funds.

Funds may have a required minimum that needs to be invested to open an account. This usually ranges from $500 to $3,000. Some may waive the minimum investment amounts if you agree to make monthly deposits to your account. Make sure you do your research.

SUMMARY

A target date fund can be a great option for any investor, from beginner to expert. It is as simple as it can get for an investment plan.

As an investor, you want to make sure you are diversified and have proper asset allocation. Target date funds offer both of those features and they are done automatically.

Although the features of this investment vehicle weigh more towards beneficial, there are some drawbacks that should be taken into consideration.

Maybe you will find a target date fund that exactly matches your needs and maybe you won’t. If you do not find an offering that suits you, remember that there are many more investment options out there.

About Post Author

Brandon Hill

I'm Brandon Hill with Bizness Professionals. We serve content to help young professionals develop personally, professionally, and financially. Well-rounded improvement is a theme we live by. As such, this website will cover a variety of topics aimed to help you have a successful life and career.