This post may contain affiliate links, which means I’ll receive a commission if you purchase through my links, at no extra cost to you. Please read full disclosure for more information.

Cash on cash return is a financial metric used in real estate transactions to measure profitability by showing total cash income earned versus total cash invested into a property.

Total cash income earned is pre-tax cash flow.

Total cash invested into the property can include the down payment, closing costs, loan fees, improvements, maintenance, and rehab fees.

This metric allows for the assessment of cash flows from income-generating assets. Its simplicity and ease of use help investors quickly compare and filter a list of potential real estate deals.

Metrics such as IRR can be more advanced for those that aren’t in the industry. When working with someone outside of real estate or finance, the cash on cash return metric is easy to understand.

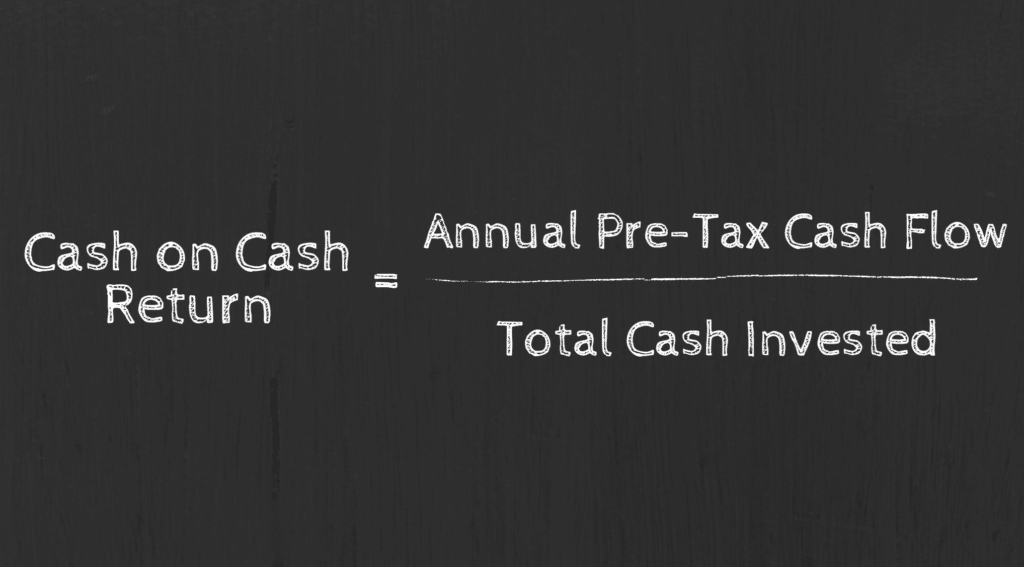

CASH ON CASH FORMULA

The formula at its core is simply cash income divided by cash invested.

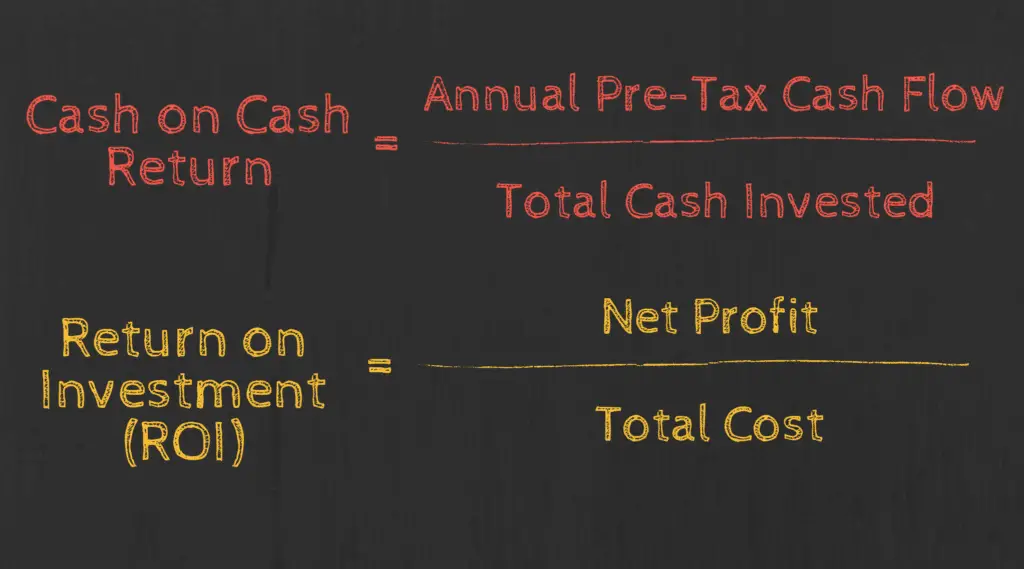

Cash on Cash Return = Annual Pre-Tax Cash Flow / Total Cash Invested

Annual Pre-Tax Cash Flow = (GSR+OI) – (V+OE+ADS)

GSR = Gross scheduled rent

- Also known as potential rental income. It represents the maximum amount of income you can expect to receive from a property through rent

OI = Other income

- All other sources of income from a piece of real estate outside of rent. (e.g. parking fees, vending machines, locker space, etc)

V = Vacancy

- Losses in income due to vacant space within the property

OE = Operating expenses

- All expenses required for the day-to-day operation of the real estate asset itself. Examples include maintenance, repairs, insurance, HOA fees, overhead costs

ADS = annual debt service

- Amount paid to cover principal and interest payments on your loan

Total Cash Invested = DP + CC + IRM

DP = Down payment

- Amount put down to acquire the property

CC = Closing costs

- The sum of all additional costs related to acquiring the property outside of the down payment

IRM = Improvements, rehab, and maintenance

- Sum of additional funds you invested into the property for improvements, rehab and maintenance

EXAMPLE: CALCULATING CASH ON CASH RETURN

Imagine that an investor purchased an office building for $1,000,000 to rent out to businesses.

The investor used a cash down payment of $200,000 and took out a loan for the other $800,000. There were another $20,000 in fees paid related to the closing of the transaction

After a year, the property brought in rental income of $120,000 and income from parking fees of $20,000.

Expenses subtracted from income included $3,600 related to vacancies, $50,000 in operating expenses, and the investor made loan payments of $30,000 for the year that was applied to principal and interest.

During the year, the investor spent $25,000 of his own money on maintenance of the property.

We’ll organize all that data with labels to begin filling in our formula for cash on cash return.

Let’s start with the numerator: annual pre-tax cash flow. Remember, its…

Annual Pre-Tax Cash Flow = (GSR+OI) – (V+OE+ADS)

Filled it with the data given from the example, this will be:

($120,000 + $20,000) – ($3,600 + $50,000 + $30,000) = $56,400

Next, let’s fill in the denominator, which was:

Total Cash Invested = DP + CC + IRM

This will be ($200,000 + $20,000 + $25,000) = $245,000.

When you put annual pre-tax cash flow over total cash invested, you get $56,400 / $245,000.

This results in a cash on cash return of 23%.

HOW TO USE AND ANALYZE THE METRIC

Understanding the number

First, let’s address what the calculated number means in plain English. If you calculate the cash on cash return to be 10%, that means the investment will earn back 10% of the cash you put into the investment for the time period you are analyzing.

Review and Project Earnings

The cash on cash calculation is best used for looking at one year of earnings from the property. These can be earnings that have already occurred or earnings you are projecting in the future.

Over the life of an investment, things will come up that will change the variables to the cash on cash return calculation. Maybe the total amount invested increases due to improvements and maintenance or maybe the property has rent escalators to increase the gross scheduled rent.

It is best practice to rerun the cash on cash return calculation when changes happen.

What is a good cash on cash return?

A good return can change depending on who you are asking. A good rule of thumb is 8-12%. Some investors may not even look at projects under a 15-20% return whereas others will happily accept 6-8%.

It is dependent on the investor’s preference, their goals, the asset, the stage of the market cycle we are in, etc.

Use as a screening tool

The cash on cash return metric is a quick and easy way to get an idea of an investment’s profitability potential.

You can use it as a quick way to screen through a large list of investments to narrow things down if you’re in a hurry. If you have more time, it is suggested to use other metrics as well, which leads us to our next point.

Use cash on cash return in tandem with other metrics

As we just stated, if you have more time to analyze real estate investments, it is recommended to use the cash on cash return as well as other metrics to fully analyze and come to a conclusion on a potential investment.

Cash on cash is not the be-all and end-all metric and it does not tell the whole story on an investment. Use other metrics such as IRR and ROI to supplement your argument for or against an investment.

Cash on cash return doesn’t take appreciation of value of the asset into consideration. If an asset has a low cash on cash return but the property is in an industry and market with substantial appreciation in value, the low cash on cash investment does not make it a bad investment.

Take everything with context.

CASH ON CASH VS ROI

The terms cash on cash return and return on investment (ROI) are often used interchangeably, leaving people wondering what the difference is between the two.

Both are return metrics used to analyze the performance of an investment.

The biggest difference between the two is that ROI measures the return on the entire amount invested whereas the cash on cash return only measures the return on out-of-pocket cash invested.

The difference between the total amount invested and out-of-pocket cash invested is the debt used.

ROI looks at the entire amount invested which is comprised of the cash you put in along with the debt used. It looks at the total wealth created by the property. This includes income generated as well as the appreciation in the value of the property.

Cash on cash return does not take into account appreciation of the property’s value. It is strictly for the cash income generated by the asset.

Example Showing Difference

Let’s say that you purchase an office building for $100,000 and sell it a year later for $110,000.

Your return on investment would be 10%. That is, your total investment of $100,000 (which can be a mix of cash and debt) has increased 10%.

If the $100,000 you purchased the office building for was funded with a $10,000 down payment of cash from your pockets and $90,000 debt, your return for the cash you invested is 100%. You put $10,000 down and gained $10,000 after 1 year.

For the sake of simplicity, this example does not show effects of vacancy, operating expenses, debt service, maintenance, etc that can affect return.

Which is better? ROI or Cash on Cash Return?

Both cash on cash return and return on investment should be used in tandem with each other.

Cash on cash return is better used for determining the stability of an asset’s income-producing ability.

For example, someone is retiring and wants an income stream to live off of. Knowing that a 15% cash on cash return on a total invested amount of $1,000,000 would produce a cash flow of $150,000 would help that person determine the stability of the stream of cash flow.

They can determine what they will receive in cash and if the investment property is able to pay itself off over time.

ROI is better for determining the total return and wealth created by an investment.

Advantages of Cash on Cash Return

Simple

- The cash on cash return is easy to calculate and wrap your head around. This is helpful for investors that may not be familiar with the lingo or math involved in real estate finance.

Quick comparisons between investments

- Investors are able to easily compare one investment against another with the cash on cash metric. Although, it should be noted that more analysis should be done before deciding or not deciding on an investment.

- Comparisons can be made between real estate investments and also against investments in other asset class types as well.

Clear picture of cash income

- This metric only looks at the returns that are driven from the cash flow of the investment property. Cash on cash does not consider the appreciation of the property’s value into account.

Can easily see the effects of leverage on return

- Real estate investors can easily test different percentages of cash versus debt they should use to achieve different levels of return. This would effect the denominator of the equation for “Total Cash Invested.”

Disadvantages of Cash on Cash Return

Taxes aren’t accounted for

- Cash on cash return is a before-tax cash flow and does not consider the effects of the investor’s tax bracket and liabilities. Taxes could greatly increase or decrease potential returns and need to be analyzed.

- A solid cash on cash return may turn unattractive after the effects of taxes.

Time value of money not accounted for

- Without taking into account the time value of money, it opens up room for the calculation to have inaccuracies. The cash on cash calculation may only be accurate for the first year.

No compound Interest

- The cash on cash calculation is based on simple interest, not compound interest. Even the slightest amount of compound interest can make an investment more attractive when comparing it to a high cash on cash return.

Ignores appreciation of the asset’s value

- A real estate investment property can provide investment value through income produced by the asset but also appreciation of the asset’s value.

- Cash on cash return only looks at the income aspect. It does not take into account the value provided by the asset appreciating. It isn’t uncommon for an asset to have poor income-producing characteristics (i.e low cash on cash return) but have a high appreciation in value.

Risk

- Risks need to be analyzed when you are judging a cash-on-cash return. A cash down payment of 10% with 90% financed with debt might help you achieve a higher cash on cash return but how much risk comes with the 90% debt?

SUMMARY

The cash on cash return is a quick and easy way to assess the income-generating ability of a real estate asset.

The inputs are easy to find and the equation is simple enough for all investors to wrap their heads around, even those not in real estate or finance.

While the metric is powerful, it should be used alongside other metrics when coming to a final decision on an investment. The cash on cash return alone does not depict the entire story of an investment.

About Post Author

Brandon Hill

I'm Brandon Hill with Bizness Professionals. We serve content to help young professionals develop personally, professionally, and financially. Well-rounded improvement is a theme we live by. As such, this website will cover a variety of topics aimed to help you have a successful life and career.