This post may contain affiliate links, which means I’ll receive a commission if you purchase through my links, at no extra cost to you. Please read full disclosure for more information.

The multi-step (short for multiple-step) income statement is the counterpart to the single-step income statement and is used by a business to report its earnings or losses for a reporting period. It is called the multi-step because of the multiple steps taken to arrive at the net income amount.

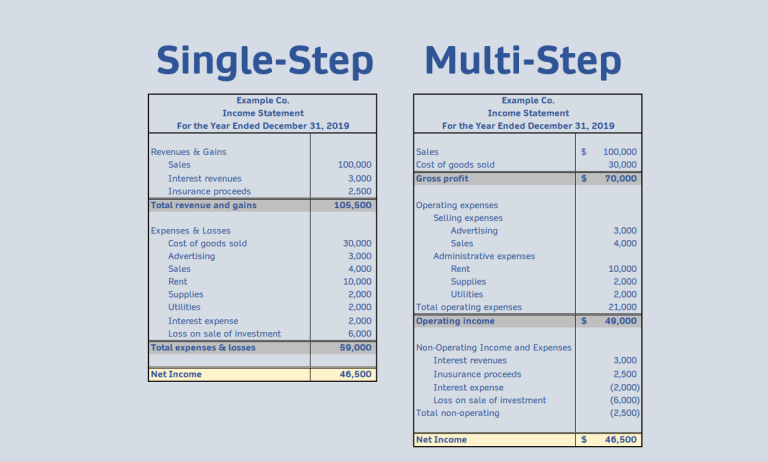

With a multi-step income statement, income, expenses, gains, and losses are categorized into operating and non-operating to show a business’s financial performance.

The multi-step income statement is prepared alongside the other two major financial statements businesses prepare: the balance sheet and statement of cash flows.

WHAT IS THE FORMAT OF THE MULTI-STEP INCOME STATEMENT?

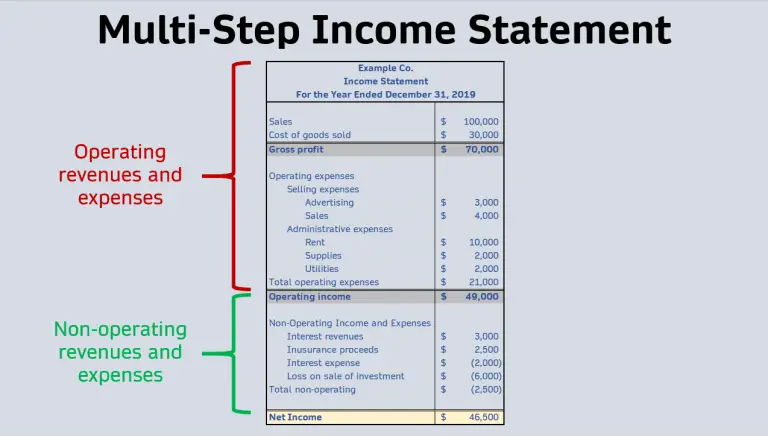

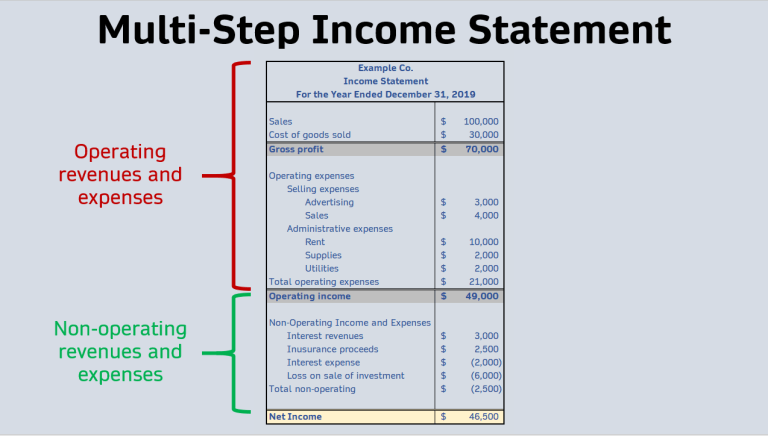

See the example of a multi-step income statement above. It is formatted with operating revenues and operating expenses separate from the non-operating revenues, non operating expenses, gains, and losses.

The separation of operating items and non-operating items make it easy to see the performance of the core business activities (operating) and what effect non-core activities had of net income (non-operating).

This layout is more detailed than a single-step income statement and tells more of the story about a company’s financial performance. With the categorization, you can analyze what drove a company’s net income. You can ask questions like…

Did they have high revenues?

Did they have low expenses?

Were the high revenues operating or non-operating?

Was the positive net income due to performance in their operating or non-operating items?

THE MULTI-STEP INCOME STATEMENT FORMULAS FOR NET INCOME CALCULATION

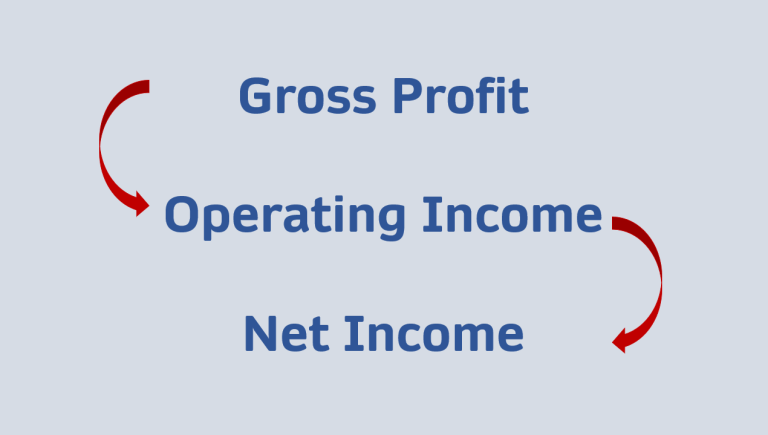

The multi step Income statement is comprised of three main formulas, which calculate 3 popular line items: gross profit, operating income, and net income.

Gross profit = Net sales – COGS

Upper management, investors, and creditors analyze gross profit since the metric shows how profitable a company is at selling the products it manufactures. Gross profit and gross profit margin, which is gross profit as a percentage of sales, may reveal the need to increase net sales or decrease costs of goods sold.

Operating Income = Gross Profit – Operating Expense

With the calculation of operating income, you are able to analyze the operations of the business. Through the operating expenses, you can determine the health of a business.

Dissect operating income and the two components of the calculation

- Why is operating income lower?

- Were operating expenses too high?

- Have they been trending upwards over time?

- Or did operating expenses remain the same, but gross profit decreased?

Asking questions like these will help you get to the root of the reasoning behind a business’s financial performance

Net Income = Operating Income + Non-operating items

Finally, when arriving at net income, you are able to see what the business’s core activities produced and what the effect of non-core activities had net income.

HOW TO PREPARE A MULTI-STEP INCOME STATEMENT

Below are 8 steps to follow in preparing a multi-step income statement:

- Choose the reporting period (monthly, quarterly, annually)

- Fill in appropriate heading information

- List Operating Revenues

- List Operating Expenses

- Calculate Gross Profit

- Calculate Operating Income

- List Non-Operating Revenues and Expenses

- Calculate Net Income

Let’s look into the details of each step.

Choose the reporting period (monthly, quarterly, annually)

An income statement always shows performance over a specific period in time. Law requires publicly traded companies to prepare one quarterly and annually.

Have you ever heard of a company “releasing earning” or having an “earnings call?” These happens once per quarter it is when companies release their financial results.

As a business owner or employee within the business, creating monthly income statements can assist in tracking how things are going

Fill in appropriate heading information

Communicate the correct information in the heading of the document. Typically, you will want:

- Company name

- Type of document (income statement)

- Reporting period

List Operating Revenues

Operating revenues are the revenues generated through the sales of your goods and service

List Operating Expenses

Operating expenses are the expenses that were incurred in the operation of your business

They include the expenses cost of goods sold, research and development, selling, general, and administrative expenses

Calculate Gross Profit

Gross profit = Net sales – COGS

Calculate Operating Income

Operating income = Gross profit – Operating expenses

List Non-Operating Revenues and Expenses

On the multi-step income statement, the non-operating sections sits below the operating section.

List out the non-operating revenues and expenses such as interest, gains and losses on asset sales, and other one-time revenues or expenses.

Calculate Net Income

Net Income = Operating Income + Non-operating items

Finally, sum up the numbers from your operating and non-operating sections to arrive at net income. A positive figure means the company earned a profit, whereas a negative figure would mean the business had a “net loss.”

SINGLE-STEP VS MULTI-STEP

Using one or the other can depend on the size and complexity of your business.

Also, who is using the income statement?

Is it for the business owners or will a bank be viewing it? Someone like a bank would want to see more detail about the business to determine your financial performance and stability.

Single-Step

- Uses one equation to calculate Net Income

- Straightforward and simple

Multi-Step

- Separates operating items and non-operating items into a 3 step process

- Offers more insight into the performance of a business

- Reports the line items gross profit and operating income

- Takes more effort to prepare

WHAT TYPES OF BUSINESSES USE MULTI-STEP INCOME STATEMENTS?

Businesses that use multi-step income statements are typically larger and more complex companies. When it comes to a publicly-traded company, they are required by law to file a multi-step income statement to give greater detail to the users of the financial statement.

Businesses that are looking to raise funds from investors and creditors are likely to use multi-step income statements as well. When you are trying to ask for money, any smart creditor or investors will want to see how your business is operating.

With the single-step layout, details are left out of the presentation and calculation of net income. The layout of the multi-step will allow the user to see the performance of the operating and non-operating components.

BENEFITS OF MULTI-STEP INCOME STATEMENTS

Multi-step income statements offer many benefits. The statement shows the line items gross profit and operating income, which are metrics commonly looked at by management, investors, and creditors.

It is a more detailed version of the single-step income statement and can lead to additional insight.

With a multi-step, you can see how well the business is performing in its main business activities and how it is performing in its other activities.

As stated in the previous section, using a multi-step income statement is beneficial when trying to attract investors or apply for credit.

DRAWBACKS OF MULTI-STEP INCOME STATEMENTS

Although the multi-step income statement comes with greater detail, it is not perfect.

The line items could be misleading if management tries to move expenses from cost of goods sold into operating expenses. This would artificially make their margins look better.

Keep an eye out in the financial footnotes of the statement and annual report, as any change like this would be disclosed there.

Creating a multi-step income statement is a labor-intensive process for a company. Accounting teams need to be robust to correctly account for the line items and classifications of revenues and expenses.

Being able to see the performance in operating items and non-operating items is a benefit if your operating items performed well.

If your operating items under performed and your non-operating items overachieved, being able to see the two can become a drawback.

If your operating income was a loss of $50 and your non-operating was a positive$100, your net income would still have been a positive $50. However, operating income can show the health of the business and when that item is decreasing or goes negative, it may raise red flags to stakeholders.

SUMMARY

The multi-step income statement is the type of income statement you are likely to see most often. Compared to the single-step income statement, the multi-step shows more insight into the performance of a business’s operations through its separation of items and additional calculations of gross profit and operating income.

About Post Author

Brandon Hill

I'm Brandon Hill with Bizness Professionals. We serve content to help young professionals develop personally, professionally, and financially. Well-rounded improvement is a theme we live by. As such, this website will cover a variety of topics aimed to help you have a successful life and career.